Personal finance can be managed with borrowings, but it becomes very important to choose among them because it affects your financial position. Because borrowing money impacts your position significantly, people have no option but to rely on either personal loans or credit cards. Both concepts differ from each other. It becomes very necessary to have knowledge about it.

Personal Loan Basics

Personal loans are term loans, and they offer you a lump sum amount at once. You have to repay it with an added rate of interest in a period ranging from 12 months to 60 months.

Important Advantages of Personal Loans

- Lower, more predictable interest rates compared with credit cards

- Easy budgeting with set payments every month

- Ideal for big expenses like house repair, medical expenses, and so on.

Nevertheless, there are some restrictions associated with personal loans, including credit verification and a relatively prolonged approval process.

Unraveling Credit Cards

Credit cards offer you a revolving line of credit. You can borrow money as and when you want. Unlike personal loans, credit cards don’t have a repayment term, which might be a risk but is also very convenient.

Main Advantages of Credit Cards

- Access money at any time whenever you need it.

- Rewards, Cash Back, and Reward Travel

- Very useful for small purchases.

- No interest charges if you pay your bill in full every month.

However, it should be noted that there are some negative consequences associated with credit cards, and these usually relate to higher rates of interest.

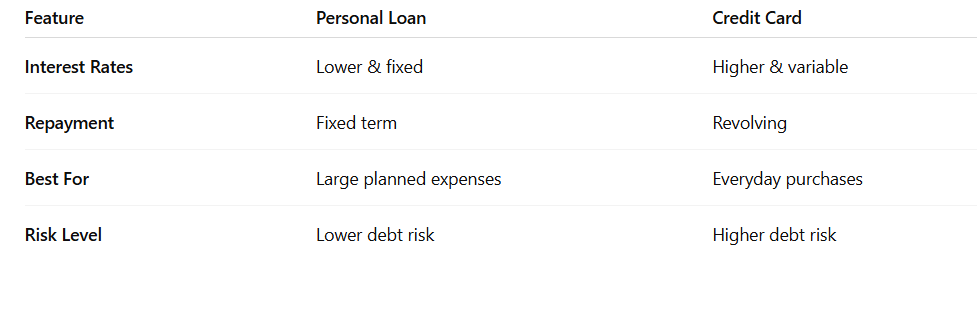

Personal Loan vs Credit Card: Key Differences

If you have been thinking about To better grasp which option works better for you, it is useful to compare and contrast these core elements:

When Should You Choose a Personal Loan?

A personal loan works best when you want a large amount of money for an intended use. For instance:

- Paying for home renovations

- Emergency Medical Bills

- Handling unexpected financial crises

- Consolidating high-interest debt

Since there is a set repayment term, you will always know exactly what you owe and exactly when the loan will be paid off.

When Should You Choose a Credit Card?

On the flip side, credit cards are preferred for short-term or smaller purchases. Credit cards have benefits and rewards that make them ideal for:

- Food, dining out, and regular expenses

- Hotel bookings

- Emergency purchases

- Earning Cash Back or Points

But if you pay your credit card bill on a regular basis and don’t let it carry an outstanding charge, credit cards should be useful for helping build credit as well as providing benefits.

Personal Loan Vs Credit Card, Which One Is Better for You?

Whether it should be an installment loan or a credit card depends on your needs.

You might want a large amount of money and rely on predictable payments. A personal loan would be a more structured option.

However, if you want convenience, easy access to money, and rewards, then a credit card might be a better option.

Tips on How to Make the Best Decision

To make sure that you make the best decision, you should follow these steps:

1. Assess your Financial Goals

Do you need it or want it?

2. Compare Interest Rates and Fees

Always make comparisons based on APRs, annual fees, and penalties.

3. Look at Your Spending Patterns

It can be useful if you’re someone who overspends and could be protected from taking on high-interest debt.

4. Check Your Credit Score

A higher credit score will afford you better terms and rates.

Conclusion

Both personal loans and credit cards can be very useful tools—when properly managed. Which is better depends on your spending behavior and your financial goals. By carefully examining and understanding the pros and cons, as well as the effects they have on your financial well-being, you will be able to make your own determination as to which option will improve your financial situation and which will have unfavorable consequences.

{kind=link}